Is Up 12.9% After Locking In GTA VI Preorder Date")

Rockstar Games and Take-Two Interactive recently confirmed that Grand Theft Auto VI preorders will open on June 25, 2026, ahead of a planned November 19, 2026 console release, easing long-running concerns about further delays.

This preorder timing, combined with intense consumer interest built up since the last GTA installment, has become central to how investors assess Take-Two’s near-term pipeline and revenue mix.

We’ll now examine how locking in the Grand Theft Auto VI preorder date could influence Take-Two’s investment narrative around growth and earnings quality.

AI is about to change healthcare. These 41 stocks are working on everything from early diagnostics to drug discovery. The best part – they are all under $10b in market cap – there’s still time to get in early.

Take-Two Interactive Software Investment Narrative Recap

To own Take-Two today, you need to believe its flagship franchises can convert years of development spend into durable cash generation, while the rest of the portfolio gradually broadens earnings beyond Grand Theft Auto. The GTA VI preorder and release dates help shore up the most important near term catalyst, but they also sharpen the key risk: heavy dependence on one launch to justify high expectations amid rising development and marketing costs.

The most relevant recent data point here is management’s FY2027 outlook, calling for US$7,900 million to US$8,100 million in revenue and a return to modest profitability. That guidance was issued before GTA VI preorder details were locked in, so investors now have a clearer line of sight on how this flagship release could interact with those targets and with other announced titles like Borderlands 4 and WWE 2K26.

Yet beneath the excitement around GTA VI, investors should be aware of how much is riding on a single release and what happens if…

Read the full narrative on Take-Two Interactive Software (it’s free!)

Take-Two Interactive Software’s narrative projects $8.8 billion revenue and $1.1 billion earnings by 2028. This requires 14.8% yearly revenue growth and a $5.3 billion earnings increase from -$4.2 billion today.

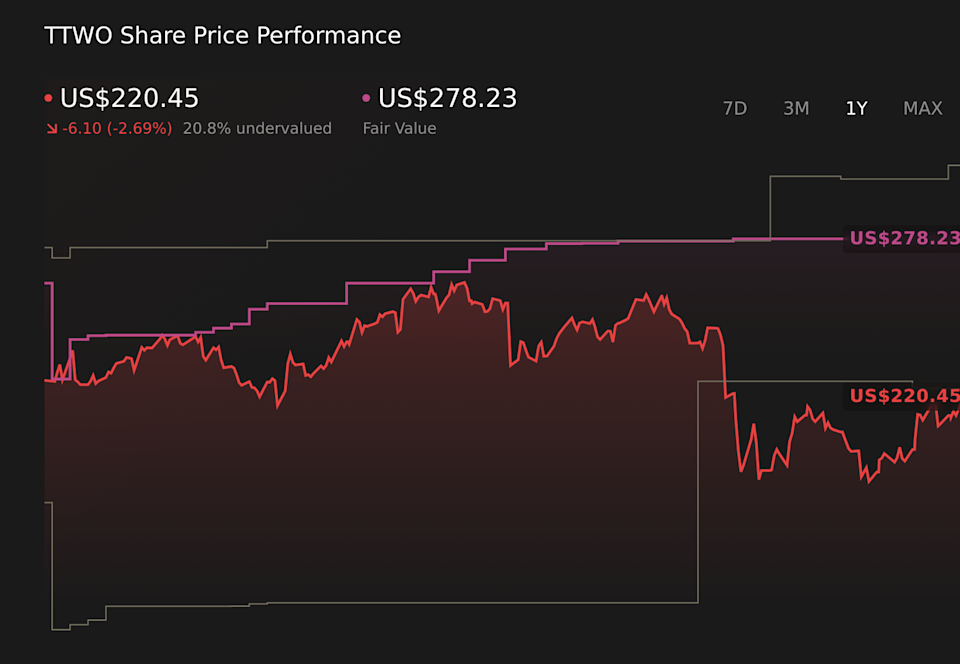

Uncover how Take-Two Interactive Software’s forecasts yield a $278.23 fair value, a 16% upside to its current price.

Exploring Other Perspectives  TTWO 1-Year Stock Price Chart

TTWO 1-Year Stock Price Chart

Some of the lowest ranked analysts paint a much more cautious picture, assuming revenue of about US$8.5 billion and earnings near US$906 million by 2029, which contrasts sharply with the concern that weak mobile trends and higher expenses could pressure margins even if GTA VI performs well. Their view highlights how sharply opinions can differ and why this preorder news could reshape both the bullish and bearish narratives from here.

Explore 9 other fair value estimates on Take-Two Interactive Software – why the stock might be worth as much as 34% more than the current price!

The Verdict Is Yours

Don’t just follow the ticker – dig into the data and build a conviction that’s truly your own.

Contemplating Other Strategies?

Early movers are already taking notice. See the stocks they’re targeting before they’ve flown the coop:

Explore 30 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

We’ve uncovered the 8 dividend fortresses yielding 5%+ that don’t just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include TTWO.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com