Valuation After New Gaming Desk And Clerkenwell Design Week Launches")

MillerKnoll (MLKN) is drawing fresh attention after Herman Miller Gaming introduced the Coyl Gaming Desk, and the wider MillerKnoll Collective rolled out new collections at Clerkenwell Design Week, putting product development firmly in focus for investors.

See our latest analysis for MillerKnoll.

Despite the recent stream of product launches, MillerKnoll’s share price has been under pressure, with a 30 day share price return of down 12.22% and a 90 day return of down 27.09%. At the same time, the 3 year total shareholder return stands at 17.11%, suggesting longer term holders have had a different experience from recent buyers.

If this mix of fresh products and mixed performance has you thinking about where else growth stories might emerge, it could be a good moment to scan 20 top founder-led companies

With MillerKnoll’s shares under pressure despite recent product momentum, the key question is whether the current valuation already reflects the company’s progress or whether the recent weakness has created a fresh entry point that anticipates future growth.

Most Popular Narrative: 52% Undervalued

At a last close of $15.45 versus a narrative fair value of $32, MillerKnoll sits at the center of a wide valuation gap that analysts link directly to future earnings power and margin recovery.

The restructuring of MillerKnoll’s reporting segments to better align with strategic goals could improve operational clarity and facilitate growth, potentially boosting revenue and net earnings by optimizing resource allocation and improving market focus.

Read the complete narrative.

Want to see what is baked into that $32 figure? The narrative leans heavily on rising margins, steadier revenue growth and a different earnings multiple than today. The detailed roadmap is laid out in the full set of forecasts and valuation assumptions, which are available for you to review in detail.

Result: Fair Value of $32 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, there are still clear watchpoints, including tariff and trade uncertainty and weaker North America Contract orders, that could easily unsettle this upside narrative.

Find out about the key risks to this MillerKnoll narrative.

Another View: Earnings Multiple Sends A Different Signal

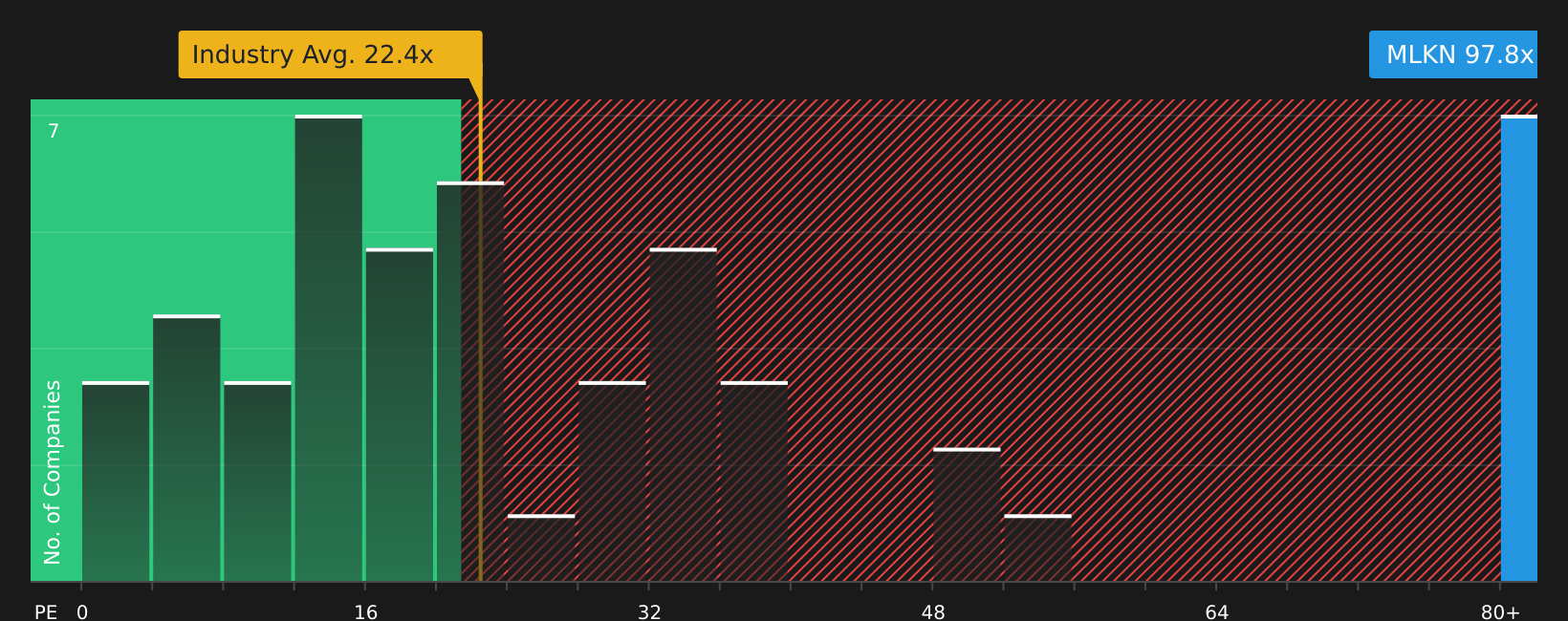

While the SWS fair value of $56.02 points to a large upside on future cash flows, the current P/E of 97.8x is very high compared with a fair ratio of 39.4x, the US Commercial Services industry at 22.4x and peers at 11.1x. This raises clear valuation risk for anyone buying today. Does the earnings multiple suggest a more cautious stance than the DCF story implies?

See what the numbers say about this price — find out in our valuation breakdown.

NasdaqGS:MLKN P/E Ratio as at May 2026Next Steps

NasdaqGS:MLKN P/E Ratio as at May 2026Next Steps

With all these mixed signals around valuation, growth potential, risks, and rewards, it makes sense to review the underlying data yourself and decide quickly what it adds up to in your view, starting with the 2 key rewards and 4 important warning signs.

Looking for more investment ideas?

If you stop with just one stock, you risk missing opportunities that suit your goals better, so take a few minutes to scan wider using focused screeners.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Try a Demo Portfolio for Free

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com