Q4 EPS Profit Challenges Bearish Loss Narratives")

Corsair Gaming (CRSR) has wrapped up FY 2025 with fourth quarter revenue of US$436.9 million and basic EPS of US$0.23, alongside net income excluding extra items of US$24.1 million, while the trailing twelve months still reflect a loss on net income and EPS. The company has seen quarterly revenue move from US$304.2 million and a basic EPS loss of US$0.56 in Q3 2024 to US$436.9 million and basic EPS of US$0.23 in Q4 2025. Trailing twelve month revenue stands at about US$1.5 billion and EPS at roughly a US$0.12 loss in the latest period. For investors watching margins and the path to sustainable profitability, the mix of quarterly profit against a still loss making twelve month profile highlights an earnings story that hinges on how efficiently Corsair Gaming can convert its sales base into durable earnings.

See our full analysis for Corsair Gaming.

With the headline numbers on the table, the next step is to set these results against the widely shared narratives around Corsair Gaming to see which stories the data supports and which ones start to look out of line.

See what the community is saying about Corsair Gaming

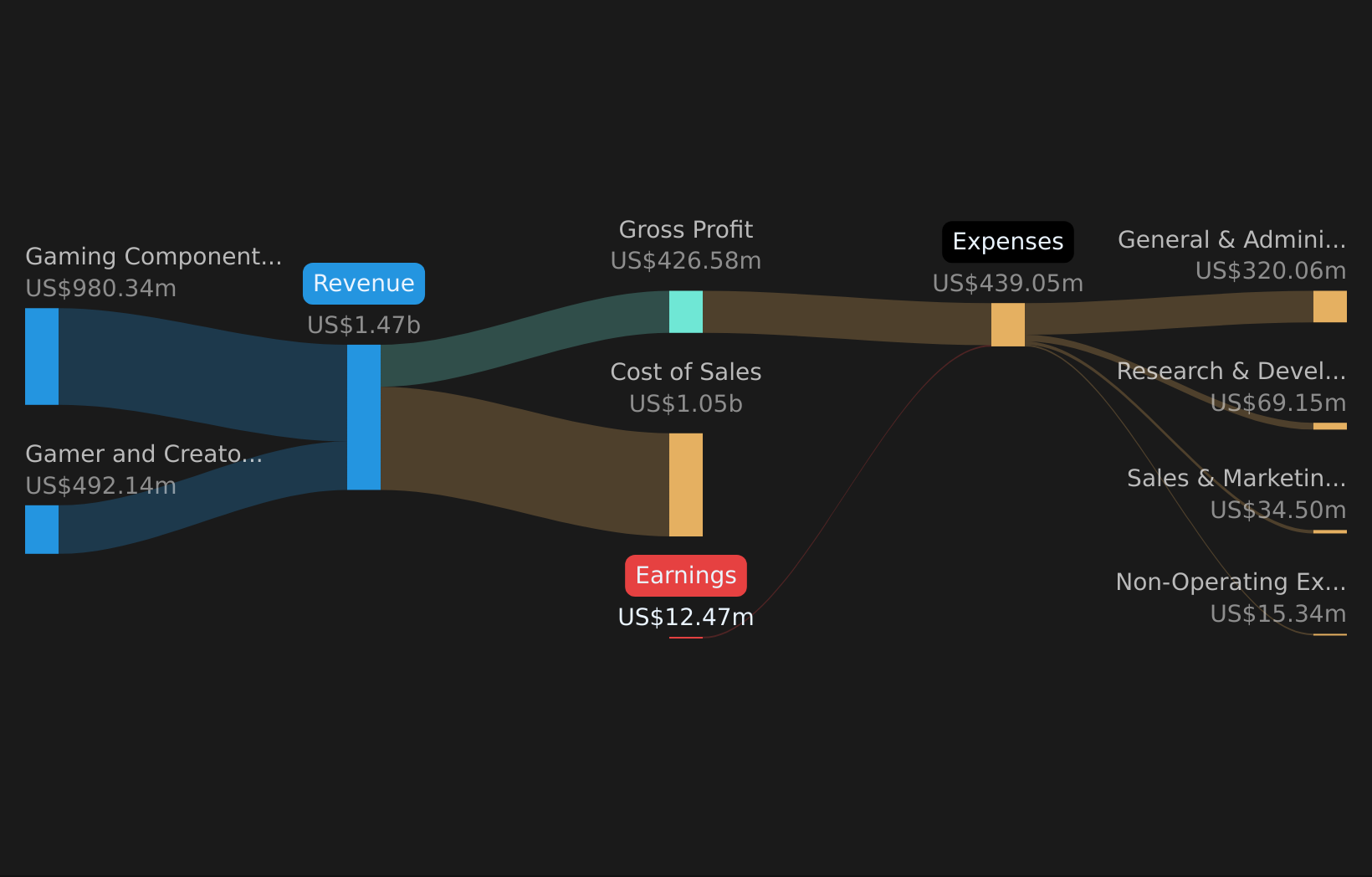

NasdaqGS:CRSR Revenue & Expenses Breakdown as at May 2026 Losses Narrow On A 12 Month View On a trailing 12 month basis, Corsair moved from a net income loss of US$99.2 million and basic EPS loss of US$0.95 at FY 2024 Q4 to a smaller loss of US$12.5 million and basic EPS loss of US$0.12 by FY 2025 Q4, alongside revenue rising from US$1.32b to US$1.47b. Consensus narrative points to earnings potentially recovering over time, and this recent shift gives mixed signals:

NasdaqGS:CRSR Revenue & Expenses Breakdown as at May 2026 Losses Narrow On A 12 Month View On a trailing 12 month basis, Corsair moved from a net income loss of US$99.2 million and basic EPS loss of US$0.95 at FY 2024 Q4 to a smaller loss of US$12.5 million and basic EPS loss of US$0.12 by FY 2025 Q4, alongside revenue rising from US$1.32b to US$1.47b. Consensus narrative points to earnings potentially recovering over time, and this recent shift gives mixed signals:

On one hand, the company is still unprofitable over the last year and historical losses have grown at about 62.6% per year, which critics highlight as a concern for earnings stability. On the other hand, forecasts referenced in the consensus view call for roughly 42.7% annual earnings growth and a path back to profitability, which is a very different picture to the trailing five year loss trend. Q4 Profit Stands Out Against Prior Quarters Within FY 2025, Q4 net income excluding extra items of US$24.1 million and basic EPS of US$0.23 contrast with losses in the first three quarters, which ranged from US$9.5 million to US$17.0 million and EPS losses between US$0.10 and US$0.16. Bulls argue that stronger product cycles and new categories can support better margins, and Q4 gives them some numerical backing and some pushback:

Support comes from the step up in quarterly revenue from US$320.1 million in Q2 2025 and US$345.8 million in Q3 2025 to US$436.9 million in Q4 2025, alongside the swing from losses to profit in that quarter. At the same time, looking at the full trailing 12 months, the company still reports a net income loss of US$12.5 million and modest trailing revenue growth of about 3.2% per year, which is below the 11.4% per year forecast for the wider US market and keeps the bullish story dependent on future rather than recent averages. Bulls who focus on Q4’s profit and the long term growth story are leaning on a narrow set of quarters, so it is worth seeing how that stacks up against a fuller bullish scenario. 🐂 Corsair Gaming Bull Case Cheap Sales Multiple Versus Ongoing Losses The stock trades around US$7.09 with a P/S of 0.5x, compared with an industry average of 2.6x and peer average of 2.2x, while the cited DCF fair value is US$8.50, about 16.6% above the current price. Bears point out that a low multiple can coexist with weak profitability, and the recent record gives them data to work with and some data that pushes back:

Supporting the cautious view, trailing 12 month revenue growth of roughly 3.2% per year and a net income loss of US$12.5 million mean the stock is still tied to a business that has not yet produced sustained profits, after several years where losses widened at about 62.6% per year. Challenging a purely bearish take, the apparent discount to the US$8.00 analyst price target and the DCF fair value of US$8.50 suggests the market is already pricing in a chunk of this risk, while forecasts cited in the analysis still call for earnings to turn positive within three years. Skeptics who see the low P/S as a warning sign often miss how much of the past loss profile might already be reflected in today’s valuation. 🐻 Corsair Gaming Bear Case Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Corsair Gaming on Simply Wall St. Add the company to your watchlist or portfolio so you’ll be alerted when the story evolves.

If the mix of risks and rewards here feels finely balanced, now may be a good time to review the numbers yourself and decide where you stand. To see both sides laid out clearly, review the 3 key rewards and 1 important warning sign

See What Else Is Out There

Corsair Gaming still reports trailing 12 month losses and relatively modest revenue growth, so the recent profitable quarter has not yet translated into consistent earnings.

If you want stocks where pricing looks more attractive relative to fundamentals, use the 51 high quality undervalued stocks now to find ideas that better align with your expectations.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Explore Now for Free

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com